This guide focuses specifically on the most damaging misconceptions that keep Minneapolis residents in debt longer than necessary, and what the legal reality actually looks like in Minnesota.

Bankruptcy Definition: Bankruptcy is a legal process established under federal law that allows individuals and businesses to restructure or eliminate qualifying debts under court supervision, providing a protected path toward financial recovery.

Debt is exhausting. Not just financially, but emotionally. The calls, the letters, the stress of watching your bank account shrink every month. And yet, a surprisingly large number of people who could qualify for bankruptcy relief sit with that burden for years, held back by things they’ve heard from friends, read in a comment section, or assumed were true. The most common mistake we see is people waiting far too long because a myth convinced them bankruptcy would destroy everything they had built.

Why Bankruptcy Myths Do Real Financial Damage

According to the United States Courts, hundreds of thousands of Americans file for bankruptcy each year and successfully emerge with a cleaner financial slate. But research consistently shows that people delay filing well past the point where it would have helped them most. That delay costs real money in mounting interest, penalties, and legal fees from creditor actions.

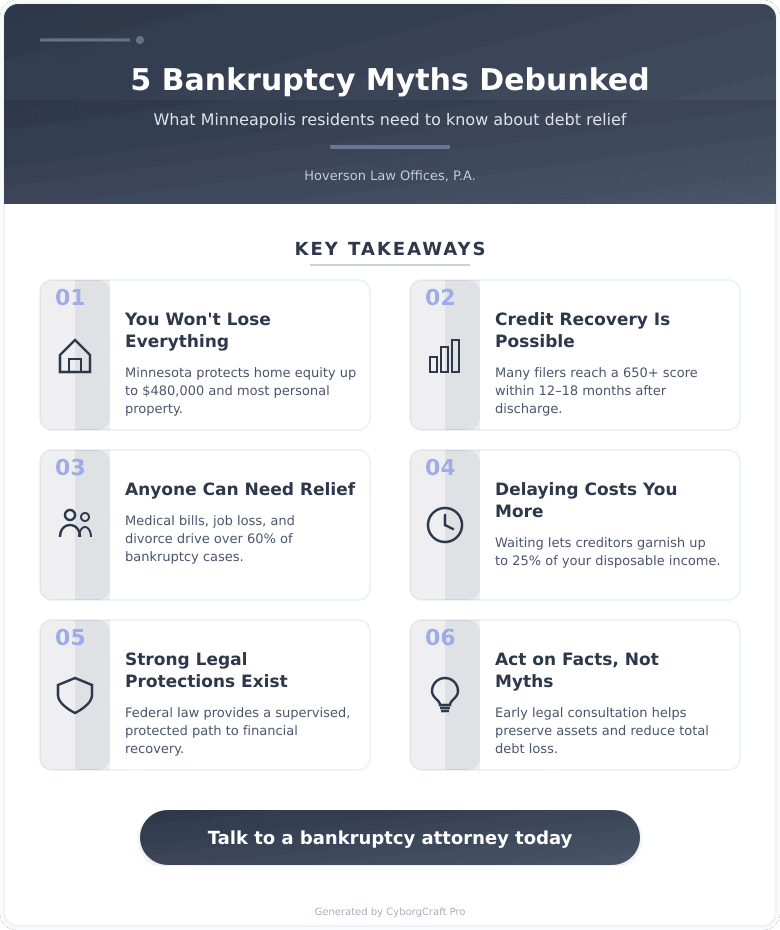

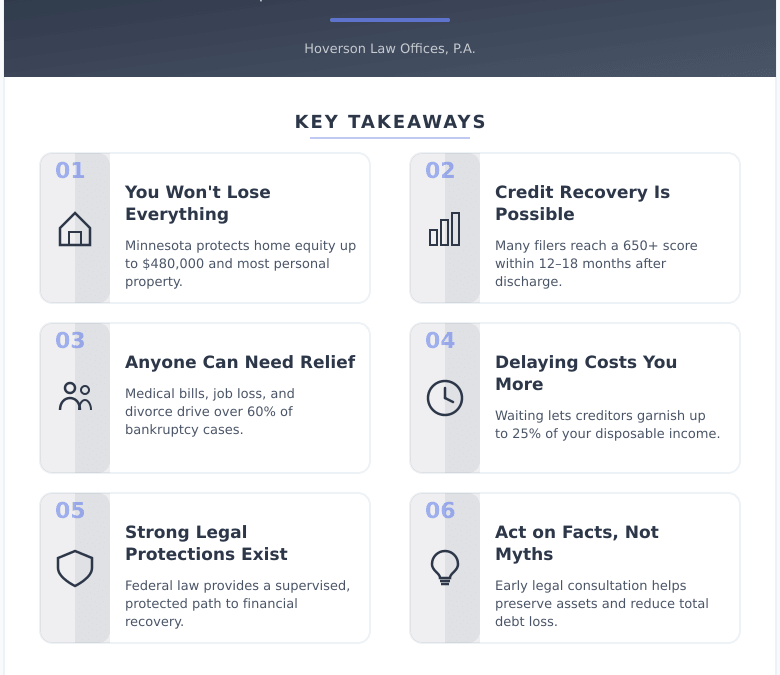

In Minnesota, wage garnishment laws allow creditors to take up to 25% of your disposable income once they have a judgment. Every month you wait while believing a myth is a month a creditor could be collecting directly from your paycheck. The pattern recognition here is consistent: by the time most people finally consult an attorney, they’ve already lost thousands of dollars they didn’t need to lose.

Firms that address these misconceptions early typically see clients preserve significantly more assets than those who come in after years of avoidance.

Thinking about whether any of this applies to your situation? Contact us for a straightforward conversation about your options. No pressure, no judgment.

The 5 Myths Holding Minneapolis Residents Back

Myth 1: You’ll Lose Everything You Own

This is the biggest one. People picture a bankruptcy trustee showing up and hauling away furniture. That’s not how it works. Minnesota has some of the more protective exemption laws in the region. Your homestead, retirement accounts, and a significant portion of personal property are often fully protected. Most people who file keep everything they own.

Minnesota Homestead Exemption: Minnesota protects up to $480,000 in home equity (or $1,200,000 for agricultural property) as of 2025, shielding your home from most creditor claims during bankruptcy proceedings.

Myth 2: Bankruptcy Ruins Your Credit Permanently

A bankruptcy filing stays on your credit report for seven to ten years depending on the type. But here’s what people miss: if you’re already carrying maxed-out cards, collection accounts, and missed payments, your credit score is likely already severely damaged. Many people see their scores begin improving within 12 to 18 months of a discharge because the debt-to-income picture clears. Recent data from credit monitoring platforms shows that post-bankruptcy filers often reach a 650+ score faster than people who spend years slowly paying down unmanageable debt.

Myth 3: Only Irresponsible People File for Bankruptcy

Medical debt is the leading driver of personal bankruptcy in the United States. Divorce, job loss, and unexpected caregiving costs follow closely behind. According to research cited by the American Journal of Public Health, over 60% of bankruptcy filers point to medical expenses as a primary cause. This has nothing to do with financial responsibility. It has everything to do with how quickly life can shift.

Myth 4: You Can’t Discharge Tax Debt or Medical Bills

Some tax debts actually can be discharged in bankruptcy if they meet specific age and filing requirements under federal law. Medical debt is generally dischargeable. The rules are specific, which is exactly why getting accurate legal guidance matters, but the blanket assumption that these debts are untouchable is simply wrong.

Dischargeable Debt: Dischargeable debt refers to qualifying obligations that a court can legally eliminate through bankruptcy, including most unsecured debts like credit cards, medical bills, and certain older tax liabilities.

Myth 5: Filing Means You’re Starting Over With Nothing

A discharge doesn’t erase your work history, your skills, your professional licenses, or your relationships. Minnesota law protects retirement accounts, tools of your trade, and basic household goods. Most people emerge from the process with a manageable fresh start, not an empty apartment and a damaged reputation.

Bankruptcy vs. Debt Settlement: Which Approach Works?

| Factor | Bankruptcy | Debt Settlement |

|---|---|---|

| Legal Protection | Immediate automatic stay stops collections | No legal protection from creditors |

| Debt Reduction | Full discharge of qualifying debts | Partial reduction, creditor must agree |

| Tax Consequences | No income tax on discharged debt | Forgiven debt may be taxable income |

| Timeline | 3-6 months (liquidation) or 3-5 years (restructuring) | 2-4 years typically |

| Credit Impact | Significant short-term, recoverable | Significant damage, unpredictable |

| Cost Range (2025) | $1,500 – $3,500 attorney fees typical | 15-25% of enrolled debt in fees |

| Best For | Overwhelming unsecured debt with legal protection needed | Smaller debt loads with cooperative creditors |

Where bankruptcy succeeds: Provides court-enforced protection immediately, resolves debt completely for qualifying filers, and offers a defined legal timeline.

Where bankruptcy has limitations: Student loans and recent tax debts are often non-dischargeable. The process is public record.

Where debt settlement succeeds: Can work for people with fewer creditors and moderate debt who want to avoid a formal filing.

Where debt settlement fails: Creditors can still sue during negotiations. Forgiven amounts may trigger a tax bill. Fees often rival bankruptcy costs.

The verdict: For most Minneapolis residents facing overwhelming debt with active collection pressure, bankruptcy provides stronger and faster legal protection than settlement programs. Settlement makes more sense for smaller, manageable balances with willing creditors.

See how your situation compares to these options. Explore our services to understand what approach fits your circumstances.

Your Debt Relief Action Plan

- Step 1 – Gather your financial picture: List all debts, creditors, income sources, and assets. Include property, retirement accounts, and vehicles. This baseline shapes every decision.

- Step 2 – Document collection activity: Save garnishment notices, judgment letters, and creditor calls. These establish urgency and inform timing.

- Step 3 – Understand Minnesota exemptions: Know what property is protected before assuming you’ll lose it. A legal consultation clarifies this in under an hour.

- Step 4 – Evaluate your debt types: Separate secured debts (mortgage, car) from unsecured debts (cards, medical). The breakdown affects which relief option fits.

- Step 5 – Consult with a Minnesota-licensed attorney: Verify credentials through the U.S. Courts website and the Minnesota State Bar. Most bankruptcy attorneys offer a free initial consultation.

Common Mistakes That Delay Relief

- Raiding retirement accounts to pay credit cards – retirement funds are often fully protected in bankruptcy, making this trade unnecessary and costly

- Transferring property to family members before filing – courts look back at transfers and can reverse them, creating legal complications

- Waiting for debt to “go away” after the statute of limitations – old debt can still harm your credit and collectors can still call

- Paying one creditor preferentially right before filing – courts can treat this as an avoidable transfer, complicating your case

At Hoverson Law Offices, P.A., located in Minneapolis, Minnesota, our approach is grounded in giving clients accurate information first so they can make real decisions about their financial future without fear or false assumptions driving the outcome.

Key Takeaways for Minneapolis Residents in 2025

- Minnesota exemptions are protective – most filers keep their home, car, and retirement accounts

- Credit recovery is possible – many people rebuild to 650+ within 12 to 18 months post-discharge

- Medical and credit card debt is usually dischargeable – don’t assume your debt type is off-limits without verification

- Waiting costs money – every month in delay can mean more garnishments, interest, and creditor judgments

- Bankruptcy and debt settlement serve different situations – the right choice depends on your specific debt profile

Frequently Asked Questions

Will I lose my house if I file for bankruptcy in Minnesota?

Not necessarily – Minnesota’s homestead exemption protects up to $480,000 in home equity as of 2025. Most homeowners who file and are current on their mortgage payments can keep their home through the process.

How long does bankruptcy stay on my credit report?

A liquidation filing stays on your credit report for ten years, while a reorganization filing remains for seven years. However, many people begin rebuilding their credit within the first 12 to 24 months after discharge.

Can bankruptcy stop wage garnishment in Minnesota?

Yes – filing triggers an automatic stay that legally halts most collection actions, including wage garnishment, immediately. This protection begins the moment you file, not after a court hearing.

How much does bankruptcy cost in Minnesota?

Attorney fees for bankruptcy in Minnesota typically range from $1,500 to $3,500 depending on the complexity of the case (2025 general market range). Court filing fees are set federally and run approximately $313 to $338. Many attorneys offer payment plans.

Are medical bills dischargeable in bankruptcy?

Yes, medical debt is generally dischargeable as unsecured debt under federal bankruptcy law. This makes bankruptcy particularly useful for people whose financial crisis started with a serious illness or unexpected hospitalization.

Do both spouses have to file if they’re married?

No – married individuals can file individually without requiring their spouse to file. Whether joint or individual filing makes more sense depends on how debt is held between spouses.

How long does the bankruptcy process take in Minnesota?

A liquidation case typically concludes in three to six months from filing date. Reorganization plans run three to five years, but the automatic stay protection begins immediately upon filing.

Your Next Step Starts Here

Debt doesn’t have to be a permanent condition. The myths surrounding bankruptcy have kept too many Minneapolis residents in financial pain longer than necessary, and the actual legal process is far less frightening than most people expect. Current best practices in debt relief show that earlier action almost always leads to better outcomes.

Ready to get real answers about your situation? Contact us today for a direct, honest conversation about what your options actually look like. No confusion, no pressure, just straight information so you can decide what’s right for you.