This guide focuses specifically on how Minnesota borrowers can understand the bankruptcy process as it relates to education debt and what legal options may actually be available to them.

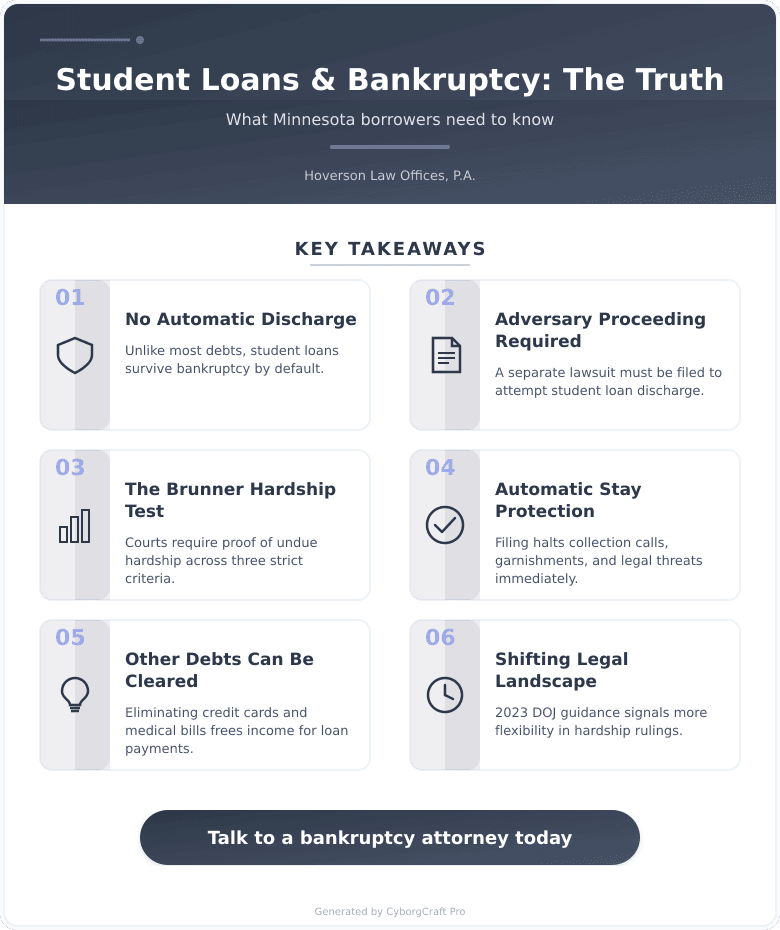

Key Definition: Discharging education debt in bankruptcy requires a separate legal action called an adversary proceeding, where the borrower must prove that repaying the debt causes an undue hardship – a standard that goes well beyond simple financial difficulty.

Why Education Debt Is Different From Other Debt

Credit card balances, medical bills, and personal loans are typically wiped out when a bankruptcy case is finalized. Education debt is not. Under federal bankruptcy law as outlined by the U.S. Courts, education debt receives a protected status that makes it far harder to eliminate.

This has been the law since 1978, and Congress has tightened the rules repeatedly since then. The result is that millions of borrowers carry this debt through financial crises that would otherwise give them a clean slate.

That said, discharge is not impossible. It is just much harder – and most borrowers never even try because they assume it can’t be done.

The most common mistake borrowers make is assuming that bankruptcy is either a complete solution or completely useless for education debt. The real answer sits somewhere in the middle, and understanding where you stand requires looking at your specific situation carefully.

What Bankruptcy Can and Cannot Do for Education Debt

Where bankruptcy helps immediately: Filing triggers an automatic stay, which stops collection calls, wage garnishment, and legal threats from creditors. This protection applies to all your debts, including education debt, while your case is active. That breathing room alone is valuable when you’re overwhelmed.

Where bankruptcy falls short for education debt: Once your case closes, the debt comes back unless you successfully filed an adversary proceeding and won. Most borrowers end the case still owing the full balance.

The verdict: Bankruptcy is a powerful tool for restructuring your overall financial picture. For education debt specifically, it works best as part of a broader strategy – not as a standalone solution. Getting rid of other high-interest debt through bankruptcy can free up income that makes your education debt more manageable.

| Debt Type | Dischargeable in Bankruptcy? | What Happens After Filing |

|---|---|---|

| Credit card debt | Yes (typically) | Eliminated when case closes |

| Medical bills | Yes (typically) | Eliminated when case closes |

| Federal education loans | Only with hardship proof | Survives bankruptcy unless court orders otherwise |

| Private education loans | Possible in some cases | Varies by loan type and court ruling |

| Tax debt | Limited (older taxes only) | Depends on age and filing status |

The Hardship Test: What Courts Actually Look At

To discharge education debt, you file a separate lawsuit within your bankruptcy case. The court then applies what’s called the Brunner test, which has three parts:

- Minimal standard of living: Repaying the debt would prevent you from maintaining a basic standard of living for yourself and your dependents.

- Persistent circumstances: Your financial situation is unlikely to improve significantly over the repayment period.

- Good faith effort: You have made genuine efforts to repay the loan before seeking discharge.

Minnesota courts apply the totality of the circumstances test strictly. Some federal courts have signaled more flexibility in how they interpret the hardship standard, and the Department of Justice updated its internal guidance in 2023 to encourage more flexibility. That trend has continued, meaning more borrowers are finding success with adversary proceedings than in previous years.

Historically, many bankruptcy filers did not attempt to discharge education debt – largely because attorneys and borrowers both assumed it was pointless. That assumption is changing as courts signal more openness to these claims.

Thinking about this for your situation? Let’s talk. Contact us and we’ll walk you through your options – no pressure.

Your Education Debt Action Plan

- Step 1 – Inventory all your debt: List every balance, interest rate, and monthly payment. Know whether your education loans are federal or private, because they are treated differently in court.

- Step 2 – Assess the full picture: Look at what bankruptcy could eliminate outside of your education debt. Removing other obligations may be enough to make your situation workable without needing discharge.

- Step 3 – Evaluate hardship eligibility: Honestly review whether you meet the three-part test. Factors like disability, long-term unemployment, or caring for a dependent with medical needs often strengthen a case.

- Step 4 – File an adversary proceeding if warranted: If hardship discharge is realistic, your attorney files a separate complaint within the bankruptcy case. This triggers a mini-trial where you present evidence.

- Step 5 – Explore income-driven repayment as a parallel option: Federal income-driven repayment programs cap payments based on earnings and forgive remaining balances after 20-25 years. These plans exist outside bankruptcy and may offer relief without court action.

Documents to gather before any consultation:

- ☐ Loan servicer statements showing current balances

- ☐ Proof of income for the past 2 years (tax returns, pay stubs)

- ☐ Monthly expense breakdown

- ☐ Documentation of any medical conditions, disability, or dependents

- ☐ Records of any repayment attempts or income-driven plan enrollment

What Minnesota Borrowers Should Know Specifically

Minnesota courts fall under the Eighth Circuit, which historically applied the Brunner test with some strictness. That said, individual judges have discretion, and outcomes vary by district. Borrowers in Minneapolis have access to the U.S. Bankruptcy Court for the District of Minnesota, which handles both Chapter 7 and Chapter 13 filings.

Minnesota does not have state-specific education debt laws that significantly alter the federal framework. However, the state does have consumer protection resources through the Minnesota Department of Commerce that can help borrowers identify servicer errors or abusive collection practices before bankruptcy even becomes necessary.

At Hoverson Law Offices, P.A., we work with people in Minneapolis and the surrounding communities who are trying to make sense of their debt situation – whether that involves bankruptcy or another path entirely. The right answer depends on the full picture, not just one piece of it.

Key Takeaways for Minnesota Borrowers in 2025

- Bankruptcy does not automatically erase education debt – a separate court action is required to attempt discharge.

- The hardship standard is real but not impossible – 2025 has brought more judicial openness to these claims than prior years.

- Private loans may be easier to discharge than federal ones in some cases, depending on how the loan was used.

- Bankruptcy still helps even without discharge – eliminating other debt frees up cash to manage education payments.

- Income-driven repayment plans are a parallel tool worth understanding before or alongside bankruptcy.

Frequently Asked Questions

Can education debt ever really be discharged in bankruptcy?

Yes, but it requires proving undue hardship through a separate legal filing called an adversary proceeding. Courts in 2025 are showing more flexibility than they did a decade ago, so more borrowers are successfully eliminating this debt than the conventional wisdom suggests.

Does filing bankruptcy stop collection on education debt?

Yes, temporarily. The automatic stay halts all collection activity – including wage garnishment and calls from servicers – while your case is active. This protection ends when the case closes unless discharge is granted.

What is the difference between federal and private education loans in bankruptcy?

Both require a hardship showing, but private loans that were used for non-qualified education expenses have been successfully discharged in some courts without the hardship standard. Federal loans are held to a stricter framework under current law.

How long does an adversary proceeding take in Minnesota?

Most adversary proceedings in the District of Minnesota resolve within 6 to 18 months, depending on complexity and whether the case is contested. Negotiated settlements with servicers sometimes resolve faster than a full trial.

Will bankruptcy ruin my credit permanently?

Bankruptcy stays on your credit report for 7 to 10 years depending on the chapter filed, but most borrowers see credit scores begin recovering within 12 to 24 months. Rebuilding credit after bankruptcy is very achievable with consistent financial habits.

What if I can’t pass the hardship test?

Bankruptcy may still help by eliminating other debt and reducing your monthly obligations, even if education debt survives. Income-driven repayment plans, refinancing, and deferment are options worth exploring alongside or instead of bankruptcy.

Ready to Understand Your Real Options?

The situation feels impossible until someone actually maps it out with you. Most people who come in believing bankruptcy is useless for education debt leave with a completely different picture of what’s possible.

Laws are shifting in 2025, courts are reconsidering old assumptions, and borrowers who were told “you can’t discharge that” are winning cases they never thought they could. You deserve accurate information before you make any decisions.

Ready to take the next step? Contact us today for straight answers and real solutions. The team at Hoverson Law Offices, P.A. serves clients throughout Minneapolis, Hennepin County, and the surrounding communities across the Twin Cities metro. For a full overview of how we can help, visit our services page.

This content is for general informational purposes only and does not constitute legal advice. Every financial situation is different. Consult a qualified attorney before making decisions about bankruptcy or debt relief.