The automatic stay is a federal legal protection that halts virtually all creditor collection actions the instant a bankruptcy petition is filed. It gives financially overwhelmed people immediate breathing room while their case moves through the court system.

This guide focuses specifically on how the automatic stay works, what it covers, what it does not cover, and how Minneapolis residents can use it to stop collection actions right now.

Automatic Stay Definition: The automatic stay is an injunction that immediately prohibits creditors, collection agencies, and courts from continuing collection efforts against a debtor the moment a bankruptcy case is filed under federal law.

The most common mistake people make is waiting. They endure months of creditor harassment, missed paychecks from wage garnishments, and sleepless nights over a looming foreclosure date – not realizing a single court filing can pause all of it. The automatic stay is not a loophole. It is a legally enforceable court order with real teeth.

What the Automatic Stay Actually Stops

The moment your bankruptcy petition is filed with the U.S. federal court system, the automatic stay goes into effect. No waiting period. No approval process. It is immediate.

Here is what it stops:

- Creditor phone calls and collection letters

- Wage garnishments and bank account levies

- Foreclosure proceedings and sheriff sales

- Vehicle repossession attempts

- Utility shutoffs (for a limited period)

- Civil lawsuits seeking money judgments

- IRS collection actions in most circumstances

Wage garnishment: A court-ordered process where a creditor takes a portion of your paycheck directly from your employer before you receive it.

Foreclosure stay: A pause on any lender’s right to sell your home through the foreclosure process, which in Minnesota can give you critical time to negotiate or reorganize debt.

Many Minnesota residents file bankruptcy each year, many specifically to trigger the automatic stay and stop active collection proceedings.

What the Automatic Stay Does NOT Cover

Honest answer: it is powerful, but not unlimited. Knowing the exceptions matters.

- Child support and alimony payments continue

- Criminal proceedings are not affected

- Certain tax audits and tax court proceedings may continue

- Student loan collection may pause but the debt itself is rarely discharged

- Creditors can file a motion to lift the stay if they have strong grounds

If a creditor believes your case was filed in bad faith, or if a secured lender (like your mortgage company) can show the property has no equity protecting other creditors, a judge can lift the stay for that specific creditor. This happens, but it requires a court hearing and takes time – time you can use.

Thinking about this for your situation? Let’s talk. The team at Hoverson Law Offices, P.A. can walk you through your options with no pressure. Contact us for a free consultation.

Automatic Stay vs. Doing Nothing: Which Approach Works?

Where the automatic stay succeeds: It stops active garnishments immediately, halts foreclosure sales that may be days away, ends collection calls legally, and gives you time to work through debt under court supervision.

Where the automatic stay has limits: It does not eliminate debt on its own. It is a pause, not a permanent fix. Some creditors can and do seek relief from the stay.

Where doing nothing succeeds: Honestly? It rarely does. Some debts do time out under statutes of limitations, and some collectors give up.

Where doing nothing fails: Wage garnishments continue indefinitely. Foreclosures proceed to completion. Bank accounts get levied. Credit damage compounds. The stress does not stop.

The verdict: For anyone facing active garnishment, imminent foreclosure, or relentless collection calls, the automatic stay is the only tool that provides legal, immediate relief. Waiting rarely improves the situation and often makes it worse.

| Situation | Without Filing | With Automatic Stay | Timeline |

|---|---|---|---|

| Wage garnishment | Continues each paycheck | Stops same day of filing | Immediate |

| Foreclosure | Proceeds to sheriff sale | Sale halted by court order | Immediate |

| Creditor calls | Continue legally | Prohibited by federal law | Immediate |

| Bank levy | Account drained | Levy action frozen | Immediate |

The 5-Step Automatic Stay Action Plan

- Step 1 – Identify Active Threats: List every active garnishment, lawsuit, foreclosure notice, or collection action currently in progress. These are your priorities.

- Step 2 – Gather Financial Documents: Collect pay stubs, tax returns, bank statements, and a full list of debts and creditors. This is what the court needs.

- Step 3 – Consult an Attorney: A bankruptcy attorney reviews your situation and confirms which type of filing triggers the stay most effectively for your circumstances.

- Step 4 – File the Petition: The moment the petition hits the clerk’s office, the stay is active. Your attorney notifies creditors immediately.

- Step 5 – Monitor for Violations: If a creditor contacts you after the stay is in place, document it. Violating the automatic stay is a federal offense and creditors can face sanctions.

Common Mistakes That Delay or Weaken the Automatic Stay

The most common mistake is filing multiple times in a short period. Under federal bankruptcy rules, if you filed a previous case that was dismissed within the last year, the automatic stay may only last 30 days – or may not apply at all. A second dismissal in 12 months eliminates it entirely unless a judge orders otherwise.

Other mistakes include:

- Incomplete paperwork that causes the case to be dismissed quickly

- Failing to notify all creditors promptly after filing

- Missing required credit counseling before filing

- Transferring assets before filing in ways that look fraudulent to a trustee

The pattern we see most often: people wait until the day before a foreclosure sale, file quickly without proper preparation, and end up with a dismissed case that limits their protection going forward. Earlier is almost always better.

What Minneapolis Residents Should Know Right Now

Minnesota follows federal bankruptcy law, so the automatic stay applies here the same way it does nationwide. What differs is the local foreclosure timeline. Minnesota uses a statutory redemption period after a foreclosure sale, which gives homeowners additional time – but that clock runs independently of the bankruptcy stay. Filing before a sheriff’s sale date preserves more options than filing after.

Hennepin County, Ramsey County, and surrounding communities including Bloomington, Plymouth, Brooklyn Park, Edina, and St. Paul all fall within the District of Minnesota federal bankruptcy court. Cases are administered through Minneapolis, which means local filings move efficiently.

At Hoverson Law Offices, P.A., located in Minneapolis, MN, our team works with residents throughout the Twin Cities area who are facing exactly these situations. We understand what local creditors do, how quickly Minnesota foreclosures move, and what the court expects from a clean filing.

See how we approach these situations – explore our services page for a full overview.

Key Takeaways for Minneapolis Residents in 2025

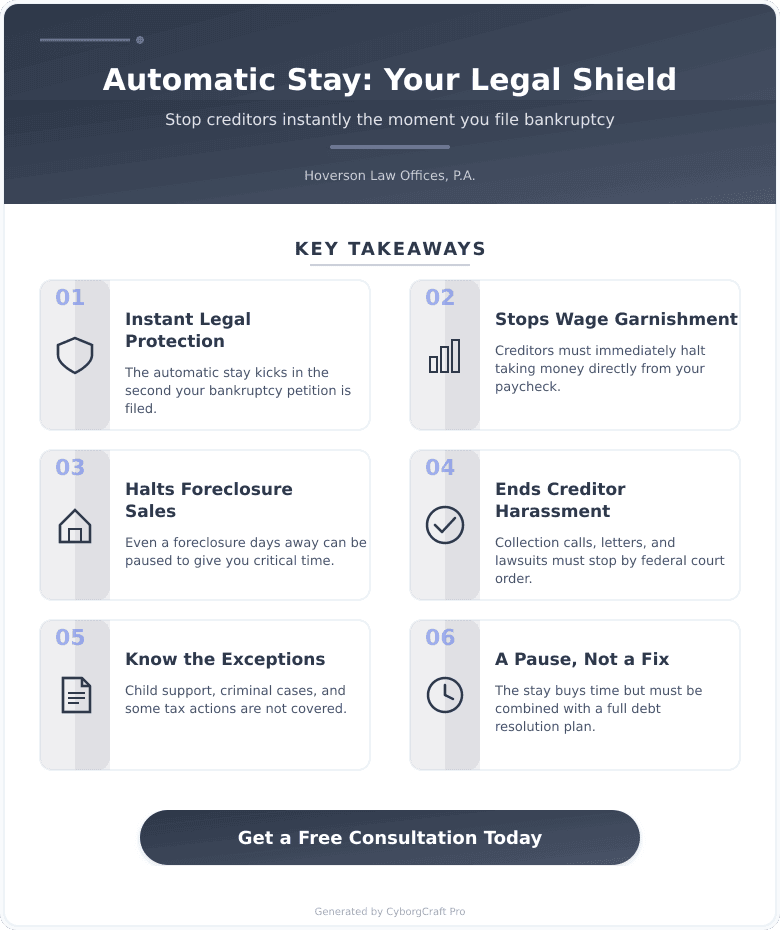

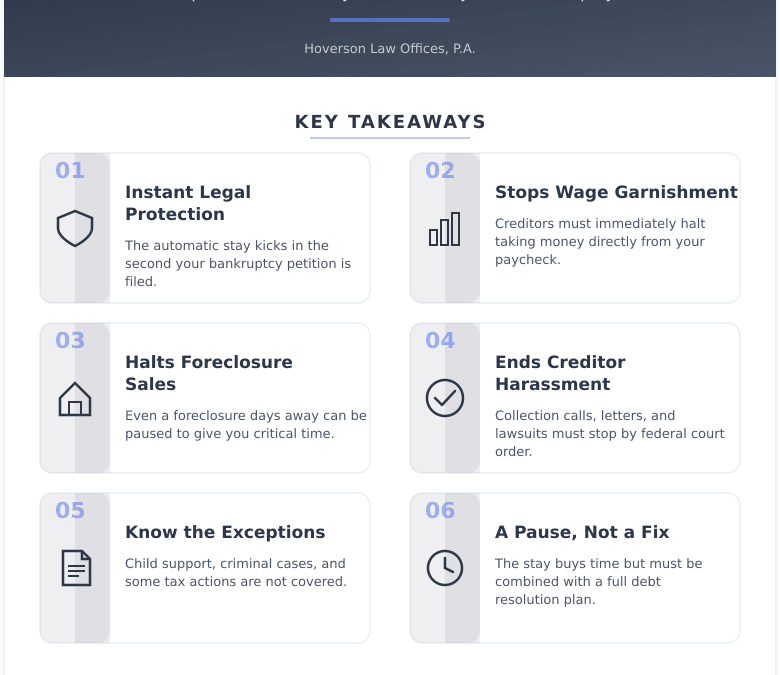

- Immediate effect – The automatic stay begins the moment your petition is filed, not after a judge reviews it

- Broad coverage – Most collection actions, garnishments, and foreclosure proceedings stop instantly

- Exceptions exist – Domestic support obligations, criminal cases, and some tax matters are not covered

- Timing matters – Filing before a foreclosure sale date preserves far more options than filing after

- Repeat filings have limits – Prior dismissed cases within 12 months can shorten or eliminate the stay in 2025

Frequently Asked Questions

How quickly does the automatic stay stop a wage garnishment?

The automatic stay stops wage garnishment the same day your bankruptcy petition is filed. Your attorney notifies your employer and the creditor, and the garnishment must cease immediately. Any wages taken after the filing date may be recoverable.

Can a creditor keep calling me after I file bankruptcy?

No – contacting you after the automatic stay is in effect is a federal violation. Creditors who continue collection calls, letters, or legal actions after filing can face sanctions from the bankruptcy court. Document any contact and report it to your attorney.

Does the automatic stay stop a foreclosure sale set for next week?

Yes, filing before the scheduled sale date halts the foreclosure proceeding immediately. The sale cannot legally proceed while the stay is active. Timing your filing correctly is critical – even a day matters.

How long does the automatic stay last?

The stay remains in effect for the duration of your bankruptcy case. In a Chapter 7 case, this typically lasts 3-6 months. In a Chapter 13 reorganization, it can last 3-5 years while you complete a repayment plan.

Can creditors get the automatic stay lifted?

Yes, creditors can file a motion asking the court to lift the stay for a specific debt or asset. A judge decides based on whether the creditor has a legitimate reason, such as a secured lender with no equity cushion in a property. This process takes time and requires a hearing.

What happens if I filed bankruptcy before and my case was dismissed?

A prior dismissed case within the last 12 months limits your automatic stay to 30 days under current federal rules. Two dismissed cases within a year eliminate the stay entirely unless you successfully petition the court for an extension. An attorney can help you navigate this before you file again in 2025.

Does the automatic stay apply to IRS collections?

In most cases, yes – the IRS must pause collection actions including levies and tax liens when the automatic stay is in place. However, the IRS can continue tax audits and assessments in many circumstances. Tax debts are also subject to specific discharge rules that differ from consumer debt.

Your Next Step

If creditors are calling daily, your paycheck is being garnished, or a foreclosure date is approaching, waiting is not a neutral choice. Every week without action is a week of continued financial damage.

Ready to stop the calls and get real breathing room? Contact Hoverson Law Offices, P.A. today for a straightforward consultation. We will tell you exactly what the automatic stay covers in your situation and what filing would mean for you – no pressure, no jargon, just honest answers.

Disclaimer: This content is for general informational purposes only and does not constitute legal advice. Every financial situation is different. Please consult a licensed attorney for advice specific to your circumstances.