This guide focuses specifically on what Minnesota borrowers misunderstand about loan consolidation and how to evaluate whether it actually makes sense for your situation.

Loan Consolidation Definition: Federal Direct Consolidation combines eligible federal loans into one loan with a weighted average interest rate rounded up to the nearest one-eighth of one percent, potentially extending repayment terms up to 30 years.

Loan consolidation comes up constantly in conversations about debt relief. And honestly, the confusion is understandable. The term sounds like refinancing, which people associate with saving money. But consolidation and refinancing are not the same thing, and mixing them up is one of the most expensive mistakes a borrower can make.

What Loan Consolidation Actually Does (And What It Doesn’t)

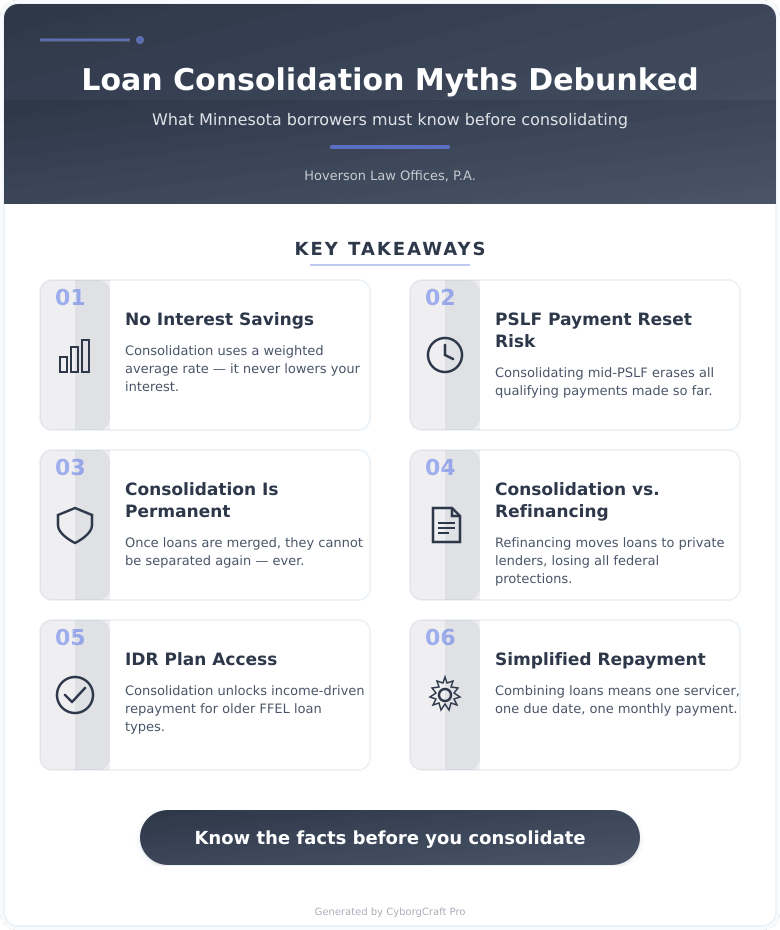

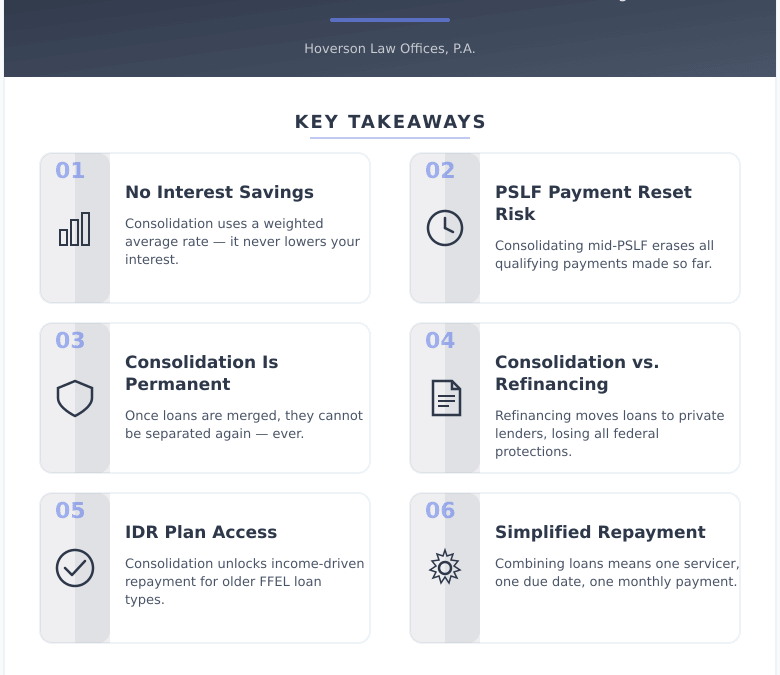

Here’s the thing most borrowers don’t realize going in: consolidation does not lower your interest rate. Your new rate is a weighted average of your existing loans, rounded up slightly. You don’t save money on interest through consolidation alone.

What it does do is simplify repayment. One servicer, one due date, one payment. For borrowers juggling four or five different loan servicers, that alone can reduce stress and prevent missed payments.

Consolidation also unlocks access to certain income-driven repayment plans (IDR plans) for older loan types like FFEL loans that don’t otherwise qualify. According to the Federal Student Aid office, consolidation is sometimes required before a borrower can enroll in income-driven repayment or pursue Public Service Loan Forgiveness (PSLF).

But here is where borrowers in Minnesota and across the country consistently get tripped up.

The Biggest Myths About Consolidation in 2025

Myth 1 – Consolidation saves you money on interest. It does not. If you want a lower rate, private refinancing is the tool for that. But private refinancing means giving up federal protections entirely.

Myth 2 – Consolidation helps with PSLF progress. This one is dangerous. Consolidating loans that already have qualifying PSLF payment history resets your payment count to zero. If you’ve made 80 payments toward forgiveness, consolidation erases that progress. The most common mistake we see is borrowers consolidating mid-PSLF track without realizing the damage until it’s too late.

Myth 3 – Consolidation and refinancing are the same thing. Consolidation keeps you in the federal system. Refinancing moves you to a private lender. That distinction matters enormously if you ever need income-driven repayment, forbearance, or forgiveness.

Myth 4 – You can unconsolidate if you change your mind. Consolidation is permanent. Once your loans are merged, you can’t separate them again.

Consolidation vs. Income-Driven Repayment: Which Approach Works?

Where consolidation succeeds: Simplifies multiple payments into one, unlocks IDR eligibility for FFEL borrowers, and allows PSLF access for previously ineligible loan types.

Where consolidation fails: Does not reduce interest rates, resets PSLF payment counts, and extends repayment timelines which increases total interest paid over time.

Where income-driven repayment succeeds: Caps payments based on income, provides forgiveness after 20-25 years, and protects borrowers during low-income periods without consolidating.

Where income-driven repayment fails: Can result in negative amortization where balances grow, forgiven amounts may be taxable, and plan availability has shifted significantly with 2025 legal challenges affecting the SAVE plan.

The verdict: For most Minnesota borrowers carrying federal loans with existing payment history, exploring IDR options before consolidating is the safer move. Consolidation makes the most sense when you hold older FFEL loans that need it to qualify for modern repayment programs.

| Option | Changes Interest Rate? | Affects PSLF Count? | Keeps Federal Protections? | Best For |

|---|---|---|---|---|

| Federal Consolidation | No (weighted avg) | Yes (resets count) | Yes | Simplifying payments, FFEL borrowers |

| Income-Driven Repayment | No | No | Yes | Managing monthly cash flow |

| Private Refinancing | Yes (potentially lower) | Yes (eliminates PSLF) | No | High-income borrowers with stable careers |

Thinking about this for your situation? Let’s talk. The team at Hoverson Law Offices, P.A. can walk you through your options with no pressure and straight answers.

Your Loan Consolidation Decision Checklist

Before you submit a consolidation application, work through this list:

- ☐ Identify every loan type you currently hold (Direct, FFEL, Perkins)

- ☐ Check your PSLF payment count through your servicer or StudentAid.gov

- ☐ Confirm whether your current loans already qualify for income-driven repayment

- ☐ Calculate how consolidation changes your repayment timeline and total interest paid

- ☐ Determine whether you work for a qualifying PSLF employer

- ☐ Review whether you need consolidation specifically to access SAVE, IBR, or PAYE

- ☐ Speak with a legal or financial professional before submitting your application

What Minnesota Borrowers Should Know Right Now

As of early 2025, the SAVE income-driven repayment plan remains tied up in federal litigation. Recent data shows that millions of borrowers enrolled in SAVE have had their payments paused while courts sort out its future. This directly affects consolidation decisions because some borrowers consolidated specifically to access SAVE, and now face uncertainty about whether that plan will survive in its current form.

Minnesota has no state-level loan forgiveness program specific to general borrowers in 2025, but healthcare workers and teachers may qualify for targeted federal programs that interact with consolidation rules in specific ways. The Minnesota Office of Higher Education tracks some state-based assistance programs worth reviewing if you work in public service.

Firms working with borrowers in Minneapolis and the surrounding Twin Cities metro area, including communities like St. Paul, Bloomington, Edina, and Plymouth, are seeing more questions about consolidation this year than in prior years. The confusion is real, and it’s understandable given how much the federal repayment system has shifted since 2024.

Key Takeaways for Minnesota Borrowers in 2025

- Consolidation does not lower your rate – it averages your existing rates and rounds up slightly

- PSLF progress resets – consolidating mid-track erases qualifying payment counts

- FFEL borrowers may genuinely need it – older loan types often require consolidation for modern IDR access

- It’s permanent – there is no way to undo a consolidation after it processes

- The 2025 SAVE litigation changes the math – get updated advice before acting on old information

Ready to take the next step? Contact us at Hoverson Law Offices, P.A. in Minneapolis, MN for straight answers about your specific loan situation. We’ll help you cut through the confusion before you make a decision you can’t reverse.

Frequently Asked Questions

Does federal loan consolidation hurt your credit score?

Federal consolidation has minimal impact on credit scores for most borrowers. It closes existing loan accounts and opens a new one, which can cause a temporary dip, but the effect is generally small and recovers quickly with consistent payments.

How long does the federal consolidation process take in 2025?

Federal Direct Consolidation typically takes 30-90 days to process after you submit your application. You continue making payments on your existing loans until consolidation is confirmed to avoid delinquency during the waiting period.

Can consolidation help if your loans are in default?

Yes, consolidation can be one path out of default for federal borrowers, but conditions apply. You generally need to agree to repay under an income-driven plan or make three consecutive voluntary payments before consolidating a defaulted loan.

What happens to your loan forgiveness timeline after consolidation?

Consolidation restarts the clock on income-driven repayment forgiveness timelines. If you were 10 years into a 20-year IDR forgiveness track, consolidating resets your progress to zero payments under the new loan.

Should high-income Minnesota borrowers consolidate or refinance privately?

High-income borrowers who don’t anticipate needing forgiveness sometimes benefit from private refinancing if they can secure a meaningfully lower rate. However, this permanently removes access to federal protections, so it’s a decision that deserves careful review with a legal professional before acting.

What is the difference between consolidation and rehabilitation for defaulted loans?

Rehabilitation removes the default notation from your credit report; consolidation does not. For borrowers in default who care about their credit record, rehabilitation followed by consolidation (if needed) is often the better sequence.

How does the 2025 SAVE plan litigation affect consolidation decisions?

Borrowers who consolidated specifically to access the SAVE plan are now in a holding pattern while federal courts decide SAVE’s future. Anyone considering consolidation for SAVE access in 2025 should wait for legal clarity or consult with a professional before acting.