This guide focuses specifically on what Minnesota borrowers need to understand about IDR plans before committing – including tax consequences, plan differences, and what recent federal changes mean for your repayment strategy in 2025.

IDR Definition: Income-driven repayment is a category of federal repayment plans that calculate your monthly payment based on your income and family size, rather than your total loan balance.

The most common mistake we see is borrowers enrolling in an IDR plan without fully understanding how interest accrual, tax liability on forgiveness, and plan eligibility changes can affect their long-term financial picture. Choosing the wrong plan – or enrolling at the wrong time – can cost you significantly over the life of the loan.

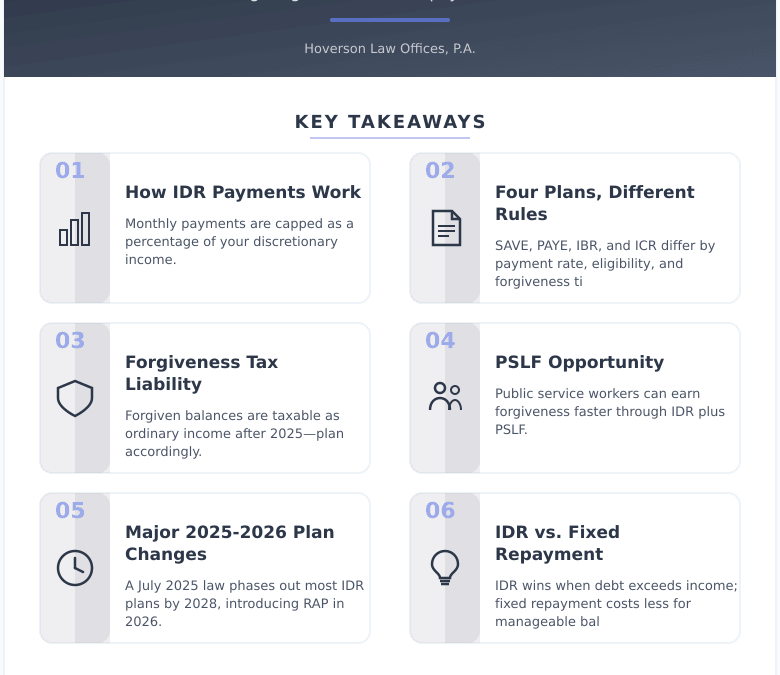

The Four IDR Plans: What Actually Separates Them

Not all income-driven plans work the same way. The federal government offers four primary IDR options (SAVE/REPAYE, PAYE, IBR, ICR) for now, but a July 2025 law introduces RAP starting 2026 and phases out most by July 2028, leaving primarily IBR and RAP. Your eligibility depends on when you borrowed and what loan types you carry.

| Plan | Payment Cap | Forgiveness Timeline | Best For |

|---|---|---|---|

| SAVE (formerly REPAYE) | 5-10% discretionary income | 20-25 years | SAVE offers 5-10% of discretionary income for many, with 20-25 year forgiveness; available to broad federal Direct Loan borrowers, but facing phase-out by 2028 under 2025 law. |

| PAYE | 10% discretionary income | 20 years | PAYE: 10% discretionary income, 20 years forgiveness, for Direct Loans first disbursed after Oct 1, 2007, to new borrowers at that time. |

| IBR | 10-15% discretionary income | 20-25 years | Most federal borrowers |

| ICR | 20% discretionary income | 25 years | Parent PLUS loan holders |

The SAVE plan has faced significant legal and legislative uncertainty, and borrowers currently enrolled in SAVE should verify their current repayment status with their servicer, as ongoing developments may affect payment processing and progress toward forgiveness.

Want to explore which plan fits your situation? Contact us for a straightforward conversation about your options – no pressure, no jargon.

Fixed Payments vs. Income-Driven Repayment: Which Approach Works?

Where fixed repayment succeeds: Predictable payments, less total interest paid over time, no tax liability at the end, and faster loan payoff for borrowers with manageable balances relative to income.

Where fixed repayment fails: Monthly payments can be unaffordable for borrowers with high debt and lower income, no safety net if income drops, and no access to Public Service Loan Forgiveness (PSLF) through standard plans.

Where IDR succeeds: Lower monthly payments free up cash for other expenses, PSLF eligibility for qualifying public service workers, and eventual forgiveness for borrowers whose balances outpace income growth.

Where IDR fails: Interest accrues significantly on lower payments, forgiven balances were excluded from federal tax through 2025 under the American Rescue Plan but are taxable as ordinary income after 2025, and plan rules can change with federal policy shifts.

The verdict: If your loan balance is less than your annual income, standard repayment usually costs less overall. If your balance significantly exceeds your annual income – especially if you work in public service – IDR paired with PSLF is often the smarter financial move. The decision depends heavily on your specific numbers, not a general rule.

What Minnesota Borrowers Should Factor In Specifically

Minnesota does not currently offer a state-level income-driven repayment program for federal loans, but the state does administer the Minnesota Office of Higher Education loan forgiveness programs for certain professionals including teachers, nurses, and public defenders. These are separate from federal IDR but can be stacked strategically.

Recent data shows that Minnesota carries one of the higher average graduate debt loads in the Midwest – borrowers here feel the weight of this decision acutely. The state income tax treatment of forgiven debt is also worth watching: while federal law currently excludes IDR forgiveness from federal income through 2025 under the American Rescue Plan provisions, Minnesota conforms to federal tax law in most cases, but that alignment is not guaranteed long-term.

Thinking about this for your situation? Let’s talk. We’ll walk you through your options – no pressure. Reach out here.

Your IDR Enrollment Action Plan

- Step 1 – Confirm your loan types: Only federal Direct Loans qualify for most IDR plans. FFEL loans require consolidation first, which resets your payment count toward forgiveness.

- Step 2 – Calculate your discretionary income: IDR payments are based on income above 150% of the federal poverty guideline for your family size. Use the Federal Student Aid Loan Simulator at studentaid.gov to model your payments accurately.

- Step 3 – Check PSLF eligibility: If you work for a government or qualifying nonprofit employer in Minnesota, run your employer through the PSLF employer search tool before choosing a plan.

- Step 4 – Project long-term tax exposure: Model what your forgiven balance might look like in 20-25 years and estimate the tax bill. That number informs whether refinancing privately might actually be cheaper overall.

- Step 5 – Recertify annually: IDR requires annual income recertification. Missing this deadline can spike your payment temporarily and cause unpaid interest to capitalize.

Documents to Gather Before You Enroll

- ☐ Most recent federal tax return or income documentation

- ☐ Your Federal Student Aid (FSA) ID and login credentials

- ☐ Complete list of all federal loan servicers and balances

- ☐ Employer information if pursuing PSLF

- ☐ Family size documentation (dependents affect your payment calculation)

Common Mistakes That Derail IDR Borrowers

Consolidating without understanding the consequences: Consolidation restarts your forgiveness clock. If you have 8 years of qualifying PSLF payments and you consolidate, you lose that progress.

Assuming all IDR plans lead to PSLF: Only certain plans qualify. ICR and IBR qualify; standard plans do not. Verify your plan qualifies before counting on forgiveness.

Ignoring interest capitalization events: When you leave a plan, miss recertification, or consolidate, unpaid interest capitalizes – meaning it gets added to your principal. That new, larger balance then accrues even more interest.

At Hoverson Law Offices, P.A., we understand how confusing federal repayment rules can be for borrowers across Minneapolis and the surrounding communities. Getting clear information early prevents costly missteps later.

Frequently Asked Questions

Will my forgiven balance be taxed as income in Minnesota?

Under the American Rescue Plan, IDR forgiveness was excluded from federal taxable income through 2025, and Minnesota generally conforms to federal tax treatment. However, forgiven balances are taxable as ordinary income after 2025, and long-term tax treatment remains subject to Congressional action. Plan accordingly.

How does enrolling in IDR affect my credit score?

Enrolling in an IDR plan does not negatively affect your credit score, as long as you make on-time payments. Your loans remain in good standing, and consistent payments can actually support your credit profile over time.

Can I switch IDR plans if my financial situation changes?

Yes, you can switch between qualifying federal IDR plans, but timing and consequences matter. Switching plans can trigger an interest capitalization event, and some switches may reset qualifying payment counts for forgiveness purposes.

What happens to my payments if my income goes up significantly?

Your monthly payment recalculates each year based on your most recent income, so higher earnings mean higher payments under IDR. If your income rises enough, your calculated payment could exceed what a standard 10-year plan would require, at which point IDR offers little advantage.

Are private loans eligible for income-driven repayment?

No – IDR plans apply exclusively to federal loans. Private loans have their own hardship programs, but they are not governed by federal IDR rules and typically offer fewer protections.

How long does IDR enrollment typically take?

Enrollment through studentaid.gov is usually processed within a few weeks, though servicer processing times vary. Submit your application well before your next payment due date to avoid any gap in coverage.

Key Takeaways for Minnesota Borrowers in 2025

- IDR is not automatically better – it depends on your debt-to-income ratio and career path

- The SAVE plan is in legal limbo – check current status before enrolling or staying in that plan

- PSLF is a separate strategy – powerful for public employees, but only with the right IDR plan

- Tax liability on forgiveness is real – model the long-term cost before assuming forgiveness is free

- Annual recertification is mandatory – missing it has real financial consequences

Your Next Step Starts Here

Federal repayment rules shifted significantly in 2024 and 2025, and more changes are likely heading into 2026. The borrowers who fare best are the ones who understand their options clearly before locking into a plan. If you have questions about how your debt fits into a broader financial or legal strategy, the team at Hoverson Law Offices, P.A. in Minneapolis, MN is ready to help you think it through.

Ready to get real answers? Contact us today and let’s have a straight conversation about where you stand and what actually makes sense for your situation.

For official federal repayment tools and plan comparisons, visit the Federal Student Aid website maintained by the U.S. Department of Education.