Bankruptcy Definition: A legal proceeding initiated under federal law that gives debtors a structured path to discharge unmanageable debt or repay it under court-supervised terms, with Minnesota courts handling filings under the U.S. Bankruptcy Code.

Most people searching for debt relief options already know things have gotten serious. Maybe collectors are calling daily. Maybe a wage garnishment just hit. The question isn’t whether bankruptcy might help – it’s which type actually fits your life. According to the United States Courts, Minnesota residents continue to evaluate both reorganization and liquidation options as income-based eligibility rules evolve.

The most common mistake we see is people assuming Chapter 7 is always faster and therefore better. That’s not always true – and picking the wrong chapter can cost you your home or your car.

The Core Difference Between the Two Paths

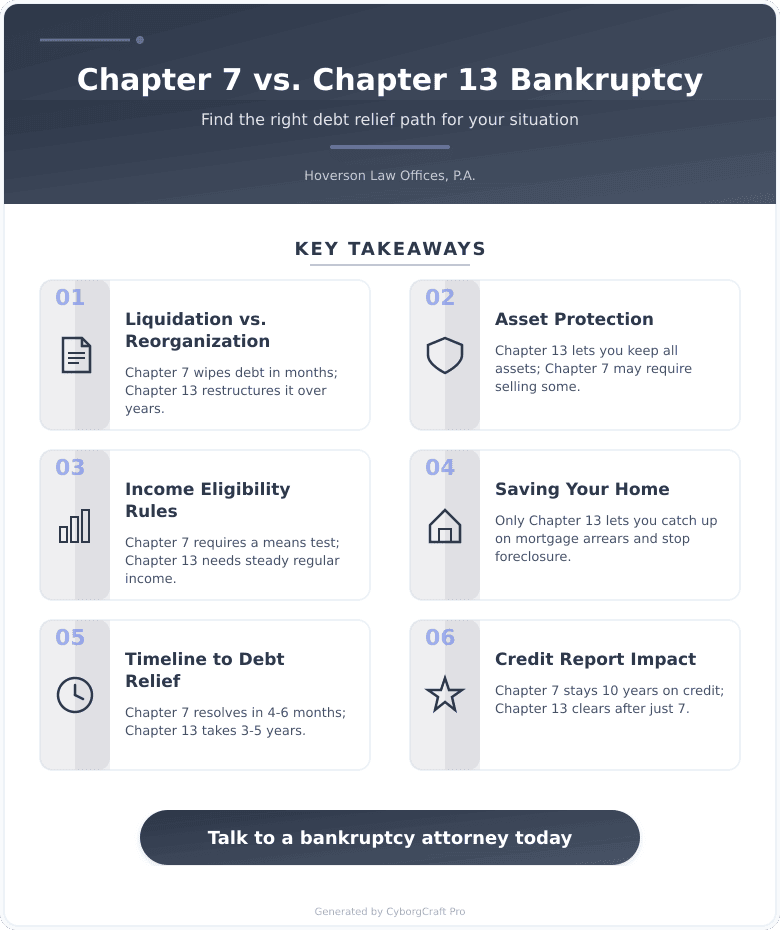

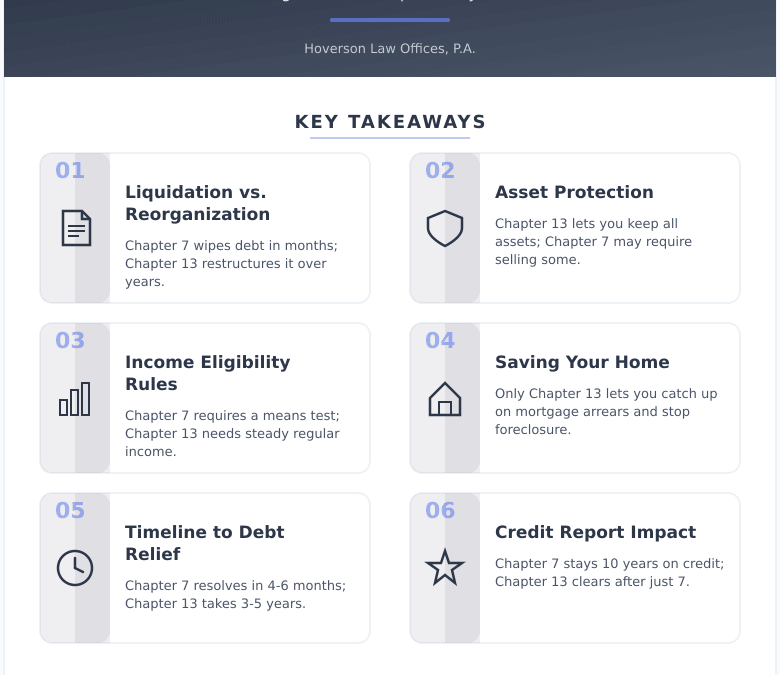

Chapter 7: A liquidation bankruptcy that wipes out most unsecured debt (credit cards, medical bills, personal loans) within 4-6 months. A court-appointed trustee may sell non-exempt assets to pay creditors.

Chapter 13: A reorganization bankruptcy where you keep your assets and repay a portion of your debt through a 3-5 year court-approved repayment plan. You must have regular income to qualify.

| Feature | Chapter 7 | Chapter 13 |

|---|---|---|

| Timeline | 4-6 months | 3-5 years |

| Asset risk | Non-exempt assets sold | Keep all assets |

| Income requirement | Must pass means test | Must have regular income |

| Mortgage arrears | Cannot cure | Can catch up over time |

| Filing fee (2025) | Filing fees vary; recent guides cite total costs around $1,500-$2,500 for Chapter 7 including attorney fees. | |

| Credit report impact | 10 years | 7 years |

| Best for | Low income, unsecured debt | Homeowners, higher income |

Chapter 7 vs. Chapter 13: Which Approach Works?

Where Chapter 7 succeeds: It discharges most unsecured debt quickly, requires no repayment plan, and gets you a fresh start in under six months. If you have limited income and few non-exempt assets, it’s often the most direct route.

Where Chapter 7 fails: It won’t stop a foreclosure long-term, can’t eliminate certain debts like recent tax obligations or child support, and requires passing a means test. If your income exceeds Minnesota’s median household income for your household size, you may not qualify.

Where Chapter 13 succeeds: It lets you catch up on mortgage arrears and save your home, protects co-signers from collections, and can strip certain junior liens in some situations. The 7-year credit report window is shorter than Chapter 7’s 10 years.

Where Chapter 13 fails: The 3-5 year commitment is long, and if your income drops or circumstances change, the plan can fail. Attorney fees are typically higher than Chapter 7 given the complexity involved.

The verdict: If you have primarily unsecured debt, limited income, and no major assets you’re trying to protect, Chapter 7 is almost always the cleaner path. If you’re behind on your mortgage and want to keep your home, or your income disqualifies you from Chapter 7, Chapter 13 is the right structure.

Thinking about this for your situation? Let’s talk. Contact us and we’ll walk you through your options – no pressure.

What Minnesota Filers Need to Know in 2025

Minnesota has specific exemptions that protect certain assets from liquidation in a Chapter 7 case. Under current Minnesota law, these include:

- Homestead exemption: Minnesota law provides a homestead exemption that protects a significant amount of home equity, with higher protections available for agricultural land

- Motor vehicle exemption: Minnesota law provides an exemption for a portion of vehicle equity

- Retirement accounts: Fully exempt under Minnesota Statutes Section 550.37

- Household goods and furnishings: Minnesota law provides an exemption for household goods and furnishings up to applicable statutory limits

- Wages: 75% of disposable earnings are protected from garnishment

Recent shifts in how Minnesota courts handle the means test calculation matter here. If your average monthly income over the six months before filing exceeds the state median, you’ll need to pass a more detailed income and expense analysis before qualifying for Chapter 7.

According to recent data from the U.S. Bankruptcy Court for the District of Minnesota, the vast majority of individual filers in the district opt for Chapter 7, though Chapter 13 filings have been trending upward as home values and mortgage arrears cases increase.

Your Bankruptcy Decision Checklist

- Step 1 – Assess your income: Compare your average monthly income over the last 6 months against Minnesota’s median. If you’re above it, Chapter 13 may be your only option.

- Step 2 – List your assets: Identify what you own and what exemptions apply. Property you’d lose in Chapter 7 might make Chapter 13 worth considering.

- Step 3 – Identify your debt type: Mostly credit cards and medical bills? Chapter 7 works well. Behind on your mortgage or car? Chapter 13 is built for that.

- Step 4 – Evaluate your timeline: Need debt relief fast? Chapter 7 resolves in months. Have income and need time to restructure? Chapter 13 gives you 3-5 years.

- Step 5 – Gather your documents: Tax returns (last 2 years), pay stubs (last 6 months), bank statements, debt statements, and property valuations.

Documents to Prepare Before Your Consultation

- ☐ Last 2 years of federal tax returns

- ☐ Pay stubs or proof of income for the past 6 months

- ☐ Bank statements (last 3 months)

- ☐ A complete list of creditors and outstanding balances

- ☐ Mortgage statements and any foreclosure notices

- ☐ Title or registration for any vehicles you own

- ☐ Recent statements for retirement or investment accounts

Key Takeaways for Minnesota Residents in 2025

- Chapter 7 is faster – most cases close within 4-6 months and discharge the bulk of unsecured debt

- Chapter 13 protects your home – it’s the only path that lets you cure mortgage arrears over time

- Minnesota exemptions are generous – especially for retirement accounts and homestead equity, which affects what you can protect

- Income determines eligibility – the means test is the first filter for Chapter 7 qualification in 2025

- Both types stop collections immediately – the automatic stay kicks in the moment you file, halting garnishments, calls, and lawsuits

Frequently Asked Questions

How long does bankruptcy stay on your credit report in Minnesota?

Chapter 7 bankruptcy stays on your credit report for 10 years, while Chapter 13 remains for 7 years from the filing date. Both affect your credit, but many filers begin rebuilding their score within a year or two of discharge through secured credit cards and consistent payment history.

What debts cannot be discharged in bankruptcy?

Neither Chapter 7 nor Chapter 13 can eliminate child support, alimony, most student loans, recent income tax debt, or criminal fines. Chapter 13 offers slightly more flexibility with certain tax obligations and student loan hardship provisions, though full discharge of student loans remains rare.

Can I keep my car if I file for bankruptcy?

Yes, in most cases you can keep your car if you’re current on payments and the equity falls within Minnesota’s applicable vehicle exemption. In Chapter 7 you’ll likely need to reaffirm the loan. In Chapter 13, you may even be able to reduce what you owe on certain vehicle loans.

How much does filing bankruptcy cost in Minnesota?

Filing fees vary; recent guides cite total costs around $1,500-$2,500 for Chapter 7 including attorney fees. Chapter 13 representation often ranges from $3,000-$4,500 given the ongoing complexity. These are general industry ranges, not specific firm rates.

Does bankruptcy stop wage garnishment immediately?

Yes – the automatic stay takes effect the moment you file, stopping wage garnishments, collection calls, lawsuits, and foreclosure proceedings. Your employer must stop the garnishment once notified of the filing, typically within a day or two.

Can I file bankruptcy more than once?

Yes, but waiting periods apply between filings. If you received a Chapter 7 discharge, you must wait 8 years before filing another Chapter 7, or 4 years before filing Chapter 13. These timelines run from the filing date of the prior case, not the discharge date.

Do I need an attorney to file bankruptcy in Minnesota?

Technically no, but self-represented filers – called pro se filers – face a significantly higher rate of case dismissal. Bankruptcy law is complex and procedural errors can delay or derail your case. Most attorneys in the Minneapolis area offer free initial consultations to evaluate your situation.

Your Next Step – Talk to Someone Who Can Actually Help

Debt doesn’t resolve itself, and the longer collections, garnishments, or foreclosure proceedings run, the fewer options you have. The automatic stay alone is one of the most powerful tools available to anyone dealing with aggressive creditors – but it only activates once you file.

At Hoverson Law Offices, P.A., we work with individuals throughout Minneapolis and the surrounding Minnesota communities to evaluate whether bankruptcy makes sense and which chapter fits their specific situation. We serve clients across Hennepin County, Ramsey County, Anoka County, and neighboring areas throughout the Twin Cities metro.

For a complete overview of how we can help, visit our services page or reach out directly.

Ready to take the next step? Contact us today for straight answers and real solutions – because the sooner you understand your options, the sooner you can move forward.