Life after bankruptcy is the period following a court-discharged bankruptcy case where your legal debt obligations are resolved and your financial recovery begins. For most Minneapolis residents, this stage brings real relief and a clearer path forward than most people expect.

This guide focuses specifically on what actually shifts in your day-to-day life after bankruptcy is discharged – and what stays the same – so you can plan realistically instead of guessing.

Life After Bankruptcy Definition: Life after bankruptcy is the post-discharge phase where a debtor’s qualifying debts are legally eliminated or restructured, and financial rebuilding begins under Minnesota state law and federal bankruptcy code.

One of the most common mistakes people make is assuming the worst about what comes next. The reality is more nuanced. Some things do change immediately. Others take time. And some things people worry about most turn out to be non-issues. At Hoverson Law Offices, P.A., we hear these questions constantly from people in Minneapolis, MN and surrounding communities – and the honest answers are worth knowing before you file, not after.

What Actually Changes After Bankruptcy Is Discharged

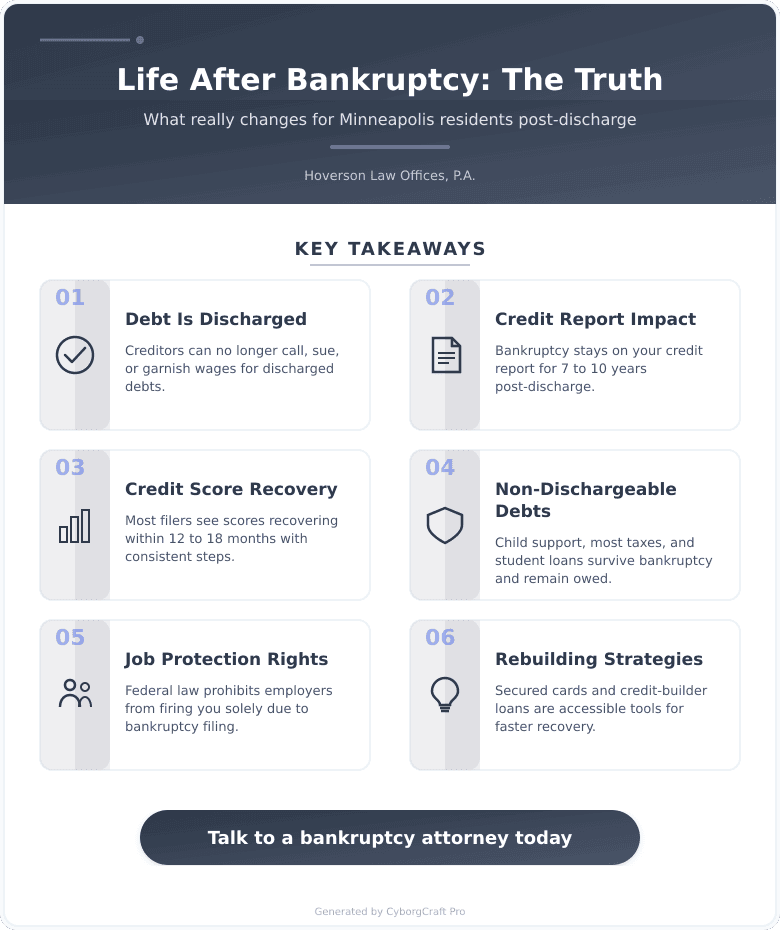

The most immediate change is simple: the debt is gone. Creditors can no longer call, sue, or garnish your wages for discharged debts. According to the U.S. Courts bankruptcy resource center, over 400,000 bankruptcy cases are filed annually nationwide, and discharge rates for eligible Chapter 7 filers exceed 95%.

Here’s what shifts right away:

- Collection calls and wage garnishments stop immediately upon filing (not just after discharge)

- Your credit report reflects the bankruptcy – typically for 7 to 10 years depending on case type

- Your debt-to-income ratio drops, which can actually improve loan eligibility faster than people expect

- Certain assets may have been liquidated or restructured during the process

Recent data shows that many bankruptcy filers see credit scores begin recovering within 12 to 18 months of discharge when they take consistent rebuilding steps. That’s not a guarantee – but it’s a reasonable benchmark based on industry patterns.

What Doesn’t Change After Bankruptcy

This is where most people are surprised. Bankruptcy doesn’t wipe the slate clean on everything.

Non-Dischargeable Debt: Certain obligations survive bankruptcy entirely and remain your responsibility after discharge.

Exempt Assets: Property protected under Minnesota exemption law that you kept during the process remains yours – and your obligations tied to it (like a mortgage you reaffirmed) continue as normal.

Things that generally do NOT go away:

- Child support and alimony obligations

- Most tax debts (with some exceptions)

- Criminal fines and restitution

- Most debts from fraud or intentional harm

- Federal and private educational loans in most cases

Your job doesn’t disappear either. Federal law prohibits most employers from firing you solely because of a bankruptcy filing. Government employers face particularly strict restrictions on using bankruptcy as a basis for employment decisions.

Thinking about this for your situation? Let’s talk. Contact us and we’ll walk you through your options – no pressure.

Rebuilding Credit in Minneapolis: DIY vs. Professional Guidance

Going It Alone vs. Working With Legal and Financial Professionals

Where going it alone succeeds: Secured credit cards, credit-builder loans through Minnesota credit unions, and on-time rent payments all help rebuild credit without outside help. These are low-cost and accessible.

Where going it alone fails: Misunderstanding what you can and can’t do post-discharge, reaffirming the wrong debts, or missing opportunities under Minnesota exemption law can set your recovery back significantly.

Where professional guidance succeeds: An attorney helps you understand exactly what was discharged, what wasn’t, and how to structure your next steps legally and strategically.

Where professional guidance fails: Cost is a real factor. Not every post-bankruptcy question requires a paid consultation.

The verdict: For the first 6 to 12 months post-discharge, at least one legal consultation is worth it. After that, credit rebuilding is largely self-directed with good financial habits.

| Factor | DIY Recovery | With Professional Help |

|---|---|---|

| Cost | Low to none | Varies by scope |

| Credit Rebuilding Speed | 12-24 months typical | Potentially faster with strategic guidance |

| Risk of Missteps | Higher | Lower |

| Best For | Straightforward discharge situations | Complex exemptions, reaffirmed debts, nondischargeable items |

Your Post-Bankruptcy Action Plan

- Step 1 – Get your discharge paperwork in order: Keep copies of your discharge order. You’ll need it to dispute errors on your credit report and to respond to any creditor contact.

- Step 2 – Pull your credit reports: Check all three bureaus within 30 days of discharge. Discharged debts should show a $0 balance and “discharged in bankruptcy” status. Dispute anything that doesn’t.

- Step 3 – Open a secured credit card: Many Minnesota credit unions offer secured cards designed for credit rebuilding. Use it for small purchases and pay it off monthly.

- Step 4 – Build an emergency fund: Even $500 to $1,000 changes how you respond to unexpected costs and keeps you out of high-interest debt cycles.

- Step 5 – Monitor your credit annually: Use annualcreditreport.com (the federally mandated free source) to track progress and catch problems early.

- ☐ Secure copies of all discharge documents

- ☐ Dispute inaccurate credit report entries within 60 days of discharge

- ☐ Open one secured credit product within 90 days

- ☐ Set up automatic payments to avoid late marks

- ☐ Review financial standing again at the 12-month mark

Frequently Asked Questions

How long does bankruptcy stay on my credit report in Minnesota?

A Chapter 7 bankruptcy stays on your credit report for 10 years from the filing date, while a Chapter 13 stays for 7 years. Minnesota follows federal Fair Credit Reporting Act rules on this timeline – there’s no state-level exception that shortens it.

Can I rent an apartment in Minneapolis after bankruptcy?

Yes, but some landlords will require larger deposits or will decline applicants with recent filings. Smaller private landlords in Minneapolis tend to be more flexible than large property management companies. Being upfront and showing post-discharge income stability helps.

Will bankruptcy affect my job in Minnesota?

Federal law prohibits government employers from discriminating against you based on a bankruptcy filing, and private employers face restrictions as well. Most employers never check. Jobs requiring security clearances or financial fiduciary roles are the main exception worth knowing about.

How soon can I get a mortgage after bankruptcy in Minneapolis?

FHA loans typically become available 2 years after a Chapter 7 discharge if you’ve rebuilt credit and meet income requirements. Conventional loans often require a 4-year wait. Local Minnesota lenders sometimes have their own overlays, so the timeline varies.

What is the most common mistake people make after bankruptcy is discharged?

The most common mistake is taking on new high-interest debt too quickly before credit is rebuilt. Predatory lenders actively target people post-discharge. Taking on a high-rate car loan or retail credit card before your score recovers can restart a debt cycle.

Does bankruptcy eliminate all my debts?

No – bankruptcy discharges qualifying unsecured debts but leaves certain obligations intact, including child support, most tax debts, and most educational loans. What gets discharged depends on your specific case type and filing details.

Can I file bankruptcy again if things go wrong after discharge?

Yes, but there are mandatory waiting periods between filings. Federal law establishes waiting periods that vary depending on the chapter previously filed and the chapter you intend to file. An attorney can confirm the specific timeframe that applies to your situation.

Key Takeaways for Minneapolis Residents in 2025

- Discharge brings real relief – collection calls, wage garnishments, and creditor lawsuits on discharged debts are legally over

- Not all debt disappears – child support, most taxes, and most educational loans survive bankruptcy

- Credit recovery is real but takes time – consistent rebuilding steps in the first 12-18 months make the biggest difference

- Employment protections exist – most employers cannot use your bankruptcy filing as grounds for termination or refusal to hire

- 2025 brings no major changes to Minnesota exemption law – the homestead exemption and personal property protections remain in place, though reviewing them with an attorney in 2026 as laws evolve is always smart

Your Next Step Starts Here

Life after bankruptcy in Minneapolis is genuinely livable – and for many people, a significant improvement over the financial stress that led to filing. The key is knowing exactly where you stand legally so you can rebuild with confidence instead of anxiety.

For a complete overview of how we can help, visit our services page. Ready to take the next step? Contact us today for straight answers and real solutions – because you’ve already done the hard part, and now it’s about moving forward clearly.