Business debt crossing into bankruptcy territory means your company’s financial obligations have grown beyond what normal operations can realistically repay, making formal legal protection a practical consideration rather than a last resort. Recognizing this threshold early gives business owners more options, not fewer.

This guide focuses specifically on Minnesota business owners who need a clear, honest look at whether their debt situation warrants a serious legal conversation.

Business Debt Crisis Definition: A state of financial distress where a company’s liabilities consistently outpace its ability to generate sufficient cash flow, leaving owners unable to meet obligations without accumulating additional debt or liquidating core assets.

A lot of Minnesota business owners hold on longer than they should, convinced that one good quarter will fix everything. From what we see serving clients in Minneapolis, MN, the warning signs usually appear months before things become truly urgent. The businesses that come out ahead are the ones that recognize those signs and act while they still have choices.

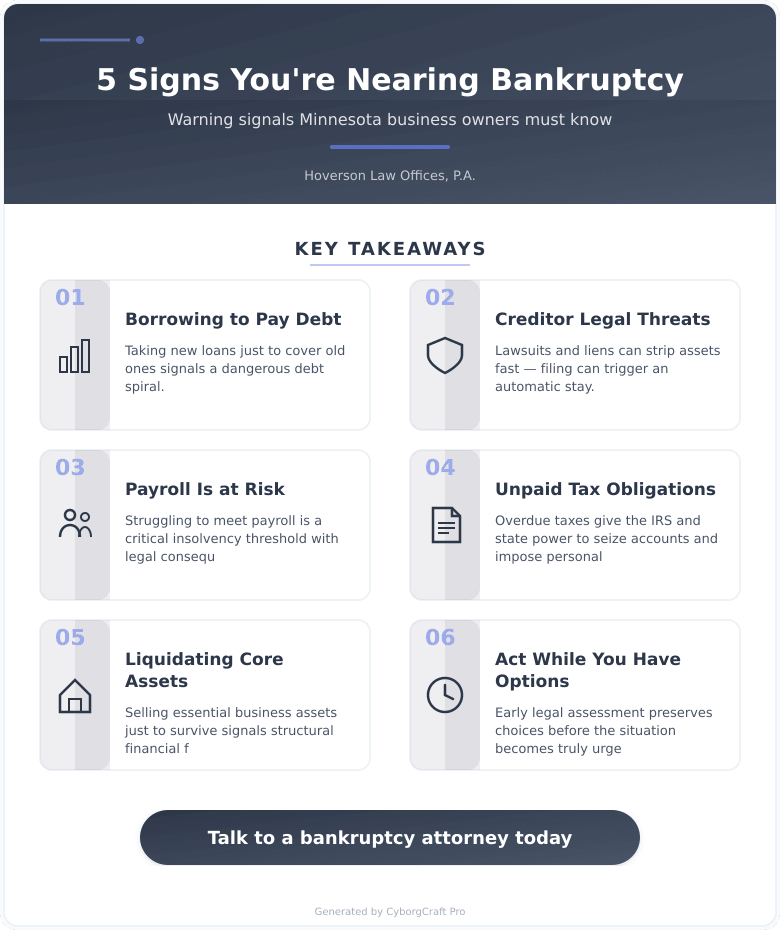

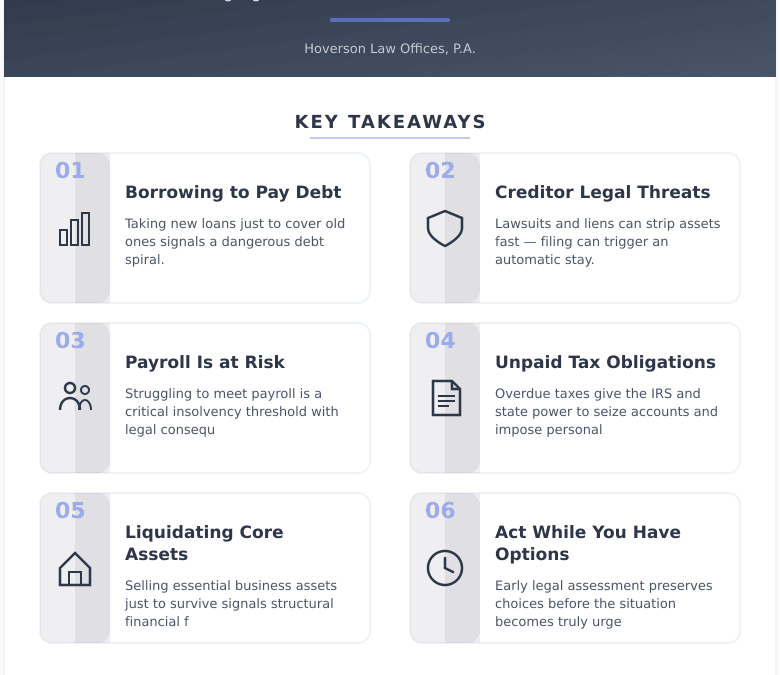

Sign 1: You Are Borrowing to Pay Previous Debt

This is one of the clearest signals. When a business takes out a new line of credit or merchant cash advance specifically to cover payments on existing loans, it has entered a debt spiral. Financial and legal professionals widely recognize compounding debt obligations as a common factor in business bankruptcy filings.

Debt spiral: A financial cycle where new borrowing is required to service prior debt, steadily increasing total obligations while reducing available cash flow.

If your business has taken on new debt two or more times in 2025 to cover old obligations, that is not a cash flow issue. That is a structural problem that needs a legal assessment.

Sign 2: Creditors Are Threatening or Initiating Legal Action

Once creditors move from phone calls to legal threats, the timeline tightens considerably. Lawsuits, wage garnishments, and liens against business property can happen fast under Minnesota law, and they can strip assets before you have any chance to organize a response.

The automatic stay in bankruptcy (a court-ordered pause on most collection actions) exists precisely for this situation. Many business owners do not realize that filing can immediately stop creditor lawsuits, foreclosure actions, and repossessions. That window matters. If creditors are already filing suit, waiting costs you leverage.

Thinking about this for your situation? Let’s talk. Contact us for a straightforward conversation about your options. No pressure, no jargon.

Sign 3: You Cannot Meet Payroll or Basic Operating Costs

Payroll is the line most business owners protect at all costs, often by neglecting vendor payments or tax obligations. But when payroll itself becomes uncertain, that is a critical threshold. Businesses that struggle to meet payroll frequently find themselves pursuing debt restructuring or other formal financial remedies in the months that follow.

Insolvency: The point at which a business can no longer pay its debts as they come due, regardless of the total asset value on paper.

Missing payroll also creates secondary legal problems in Minnesota, including potential personal liability for unpaid employment taxes. This is the kind of compounding risk that makes early action so much more practical than waiting.

Sign 4: Tax Obligations Have Gone Unpaid for Multiple Periods

Unpaid payroll taxes, sales taxes, and state income taxes are not like ordinary vendor debt. The IRS and the Minnesota Department of Revenue have collection tools that most creditors do not, including the ability to seize business bank accounts and hold owners personally liable in many circumstances.

Under current Minnesota law (2025), the state can assess trust fund recovery penalties personally against owners and officers when payroll taxes go unremitted. If your business has accumulated two or more periods of unpaid tax obligations, that is a sign the financial situation has moved well beyond routine cash flow management.

Sign 5: You Have Stopped Opening Financial Statements

This one sounds simple, but it carries real weight. When business owners stop reviewing bank statements, income reports, or aging receivables, it is usually because the numbers are painful and the path forward is unclear. That avoidance has a cost. Businesses that delay recognizing insolvency often lose options that were available months earlier.

The most common pattern we see is an owner who has a rough sense things are bad but has not confirmed the actual numbers in weeks or months. That gap between instinct and data is where opportunities to act get missed.

Restructuring vs. Liquidation: Which Path Fits Your Situation?

| Factor | Restructuring (Reorganization) | Liquidation (Wind-Down) |

|---|---|---|

| Business continues? | Yes | No |

| Typical timeline | 3-5 years (repayment plan) | 3-6 months |

| Best for | Viable business, temporary distress | Business no longer sustainable |

| Effect on personal assets | Generally protected if structured properly | Depends on entity type and guarantees |

| Creditor negotiations | Court-supervised repayment | Asset distribution by priority |

Where restructuring succeeds: Businesses with consistent revenue, loyal customers, and fixable cost structures can often reorganize and survive intact.

Where restructuring fails: If the core business model is broken or market demand has evaporated, reorganization only delays the inevitable.

Where liquidation succeeds: It provides a clean, legally protected exit that stops creditor harassment and resolves personal guarantee exposure in many cases.

Where liquidation fails: Owners who liquidate too late often find that asset values have dropped significantly, leaving less for creditors and more personal exposure.

The verdict: If your business generates real revenue and has a path to profitability without the current debt load, restructuring is worth serious consideration. If the business model itself is the problem, a structured wind-down protects you better than fighting indefinitely.

See how our approach to business debt situations compares. We walk you through the options honestly before you commit to anything.

Your Business Debt Action Plan

- Step 1 – Get the real numbers: Pull your last three months of bank statements, tax filings, and a full creditor list with balances. You cannot make a good decision without accurate data.

- Step 2 – Identify which debts carry personal guarantees: Many Minnesota business owners do not realize they are personally liable for certain business debts until collection starts. Know your exposure now.

- Step 3 – Stop taking on new debt to cover old obligations: Each new obligation reduces your restructuring options and increases total liability.

- Step 4 – Document all creditor communications: Letters, emails, lawsuit notices. This record matters enormously if you pursue legal protection.

- Step 5 – Schedule a legal consultation before the situation escalates: Options available today may not be available in 90 days. Acting while you still have flexibility is the single most valuable thing you can do.

What Minnesota Business Owners Should Gather Before a Consultation

- ☐ Complete list of creditors with outstanding balances

- ☐ Last 3 months of business bank statements

- ☐ Any active or threatened lawsuits, liens, or garnishments

- ☐ Most recent business tax returns (federal and Minnesota state)

- ☐ List of business assets (equipment, inventory, receivables)

- ☐ Copies of any personal guarantees signed for business debt

- ☐ Payroll records showing any missed or delayed payments

Key Takeaways for Minnesota Business Owners in 2025

- Early action preserves options – legal protections available today narrow significantly once creditor lawsuits are filed.

- Personal liability is real – unpaid payroll taxes and personal guarantees can follow you past the business itself.

- Restructuring is not failure – many viable Minnesota businesses have reorganized and recovered when the underlying operations were sound.

- The automatic stay is powerful – filing can immediately halt collection actions, giving you breathing room to assess next steps.

- Avoidance has a cost – every month without a clear plan typically reduces the range of available solutions.

Frequently Asked Questions

How do I know if my business debt qualifies for bankruptcy protection?

Any business that cannot meet its financial obligations as they come due may qualify for bankruptcy protection, regardless of total debt amount. Minnesota businesses can file under several federal bankruptcy chapters depending on structure and goals. A legal assessment of your specific situation determines which options apply.

Will filing for business bankruptcy affect my personal credit in Minnesota?

Whether business bankruptcy affects personal credit depends heavily on how the business is structured and what personal guarantees exist. Sole proprietors and partners often face personal impact, while properly structured corporations or LLCs may limit personal exposure. Personal guarantees on business loans complicate this considerably.

How long does a business bankruptcy process typically take in Minnesota?

Business bankruptcy timelines in Minnesota range from roughly 3-6 months for liquidation to 3-5 years for a full reorganization plan. Emergency protections like the automatic stay take effect within hours of filing, which is often the most immediate benefit for businesses under active creditor pressure.

What is the difference between business debt restructuring and bankruptcy?

Debt restructuring is a negotiated process between a business and its creditors, while bankruptcy is a formal legal process supervised by a federal court. Restructuring can happen outside of court but lacks the automatic stay protection. Bankruptcy provides legal enforceability that informal negotiations cannot guarantee.

Can I keep my business open while going through bankruptcy in 2025?

Yes, certain bankruptcy filings allow businesses to continue operating while reorganizing under court supervision. The business keeps generating revenue, fulfilling contracts, and paying employees during the process while a repayment plan is developed and approved.

What happens to employees if a Minnesota business files for bankruptcy?

Employee wages and benefits often receive priority status in bankruptcy proceedings, meaning they are paid before many other creditor claims. Whether employees keep their jobs depends on whether the business is reorganizing or winding down, but their unpaid wages generally carry strong legal protection under federal bankruptcy law.

What This Means for Minneapolis Business Owners Right Now

If any of the five signs in this post describe your current situation, the worst thing you can do is wait. The gap between “this is manageable” and “we’ve run out of options” closes faster than most people expect, especially as 2025 interest rates keep pressure on operating costs across Minnesota.

At Hoverson Law Offices, P.A., we work with business owners throughout Minneapolis and the surrounding Twin Cities metro who are trying to make honest, informed decisions about serious debt situations. There is no judgment here and no pressure. Just straight answers about what your options actually are.

Ready to take the next step? Contact us today for a real conversation about your situation. The sooner you understand your options, the more of them you will still have.

This content is intended for general informational purposes only and does not constitute legal advice. Please consult with a qualified attorney regarding your specific legal situation.