This guide focuses specifically on borrowers in or approaching default who need to understand the timeline, consequences, and concrete options for stopping the financial fallout before it gets worse.

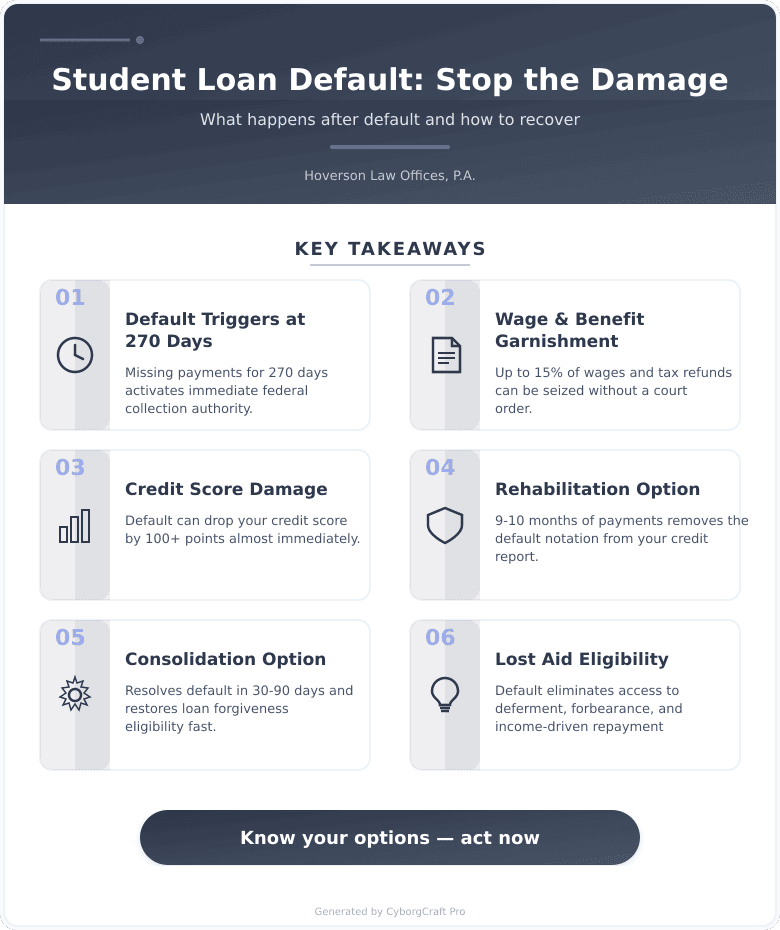

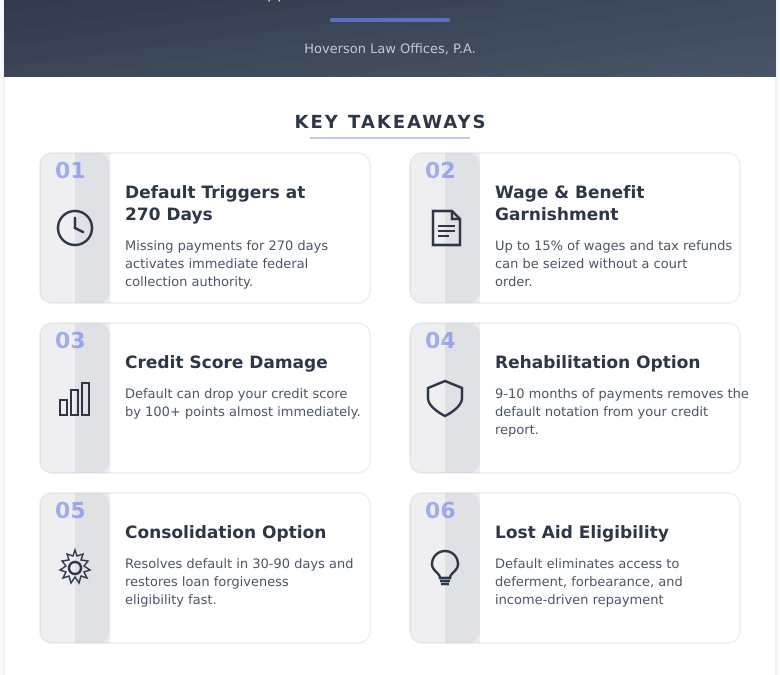

Default Definition: Federal loan default occurs when payments are missed for 270 consecutive days, triggering immediate collection authority by the U.S. Department of Education including wage garnishment, tax refund seizure, and credit damage.

If your loans have crossed into default – or you’re close – the situation feels overwhelming. But it’s not permanent. There are real options available in 2025, and understanding exactly what happens next is the first step toward stopping the damage.

What Default Actually Triggers – The Full Picture

Most borrowers don’t realize how fast consequences pile up after default is declared. Within weeks, you can expect:

- Your entire loan balance becomes due immediately, not just missed payments

- The account is referred to a collections agency or the Department of Education’s internal collectors

- Your credit score drops significantly – often 100 points or more

- Your wages can be garnished without a court order (up to 15% of disposable income)

- Federal and state tax refunds can be seized through the Treasury Offset Program

- Social Security benefits can be offset if you’re a retired or disabled borrower

Treasury Offset Program: A federal collection tool that allows the government to intercept tax refunds, Social Security payments, and other federal benefits to satisfy defaulted loan balances.

According to the Federal Student Aid office, defaulted borrowers also lose eligibility for federal financial aid, deferment, forbearance, and income-driven repayment plans – removing the very tools that could have helped earlier.

The most common mistake borrowers make is assuming default is too far gone to fix. That thinking keeps people stuck when real solutions exist right now.

Rehabilitation vs. Consolidation: Which Approach Works?

Two main federal programs help borrowers exit default. Choosing the right one matters.

Where Rehabilitation succeeds: It removes the default notation from your credit report entirely (though late payment history stays). It restores eligibility for income-driven repayment. It’s available once in a borrower’s lifetime and typically takes 9-10 months of agreed-upon payments.

Where Rehabilitation fails: It takes nearly a year before default status is cleared. Wage garnishment may continue during the process. Collection fees of up to 16% can be added to your balance.

Where Consolidation succeeds: It resolves default faster – sometimes in 30-90 days. You can combine multiple loans into one. It restores access to income-driven plans and Public Service Loan Forgiveness immediately upon completion.

Where Consolidation fails: The default notation stays on your credit report for seven years. You can only use consolidation to exit default if you agree to an income-driven repayment plan or make three consecutive voluntary payments first.

The verdict: Borrowers focused on credit recovery should pursue rehabilitation. Borrowers who need fast resolution – especially those working toward loan forgiveness programs – should consolidate. Your specific loan types and financial goals determine which fits better.

| Option | Time to Exit Default | Credit Impact | Eligibility Restored | Best For |

|---|---|---|---|---|

| Rehabilitation | 9-10 months (2025) | Default removed from report | Yes, after completion | Credit repair priority |

| Consolidation | 30-90 days (2025) | Default stays 7 years | Yes, immediately after | Fast resolution, forgiveness paths |

| Full Repayment | Immediate upon payment | Default removed | Yes | Borrowers with lump sum available |

Thinking about this for your situation? Let’s talk. Contact us and we’ll walk you through your options – no pressure, just straight answers.

Your Default Recovery Action Plan

- Step 1 – Confirm your loan status: Log into studentaid.gov to identify your servicer, loan types, and exact balance. Private loans operate under different rules than federal loans – this distinction changes everything.

- Step 2 – Stop any active garnishment: Contact your loan holder immediately. Voluntary payments during rehabilitation can sometimes reduce or suspend garnishment depending on your agreement.

- Step 3 – Choose rehabilitation or consolidation: Use the comparison above and your specific goals to decide. Contact your servicer or the Default Resolution Group at 1-800-621-3115 to begin.

- Step 4 – Get on an income-driven plan: After exiting default, enroll in an income-driven repayment plan. Payments can be as low as $0 depending on income. This prevents re-default.

- Step 5 – Protect your credit going forward: Request written confirmation once default is resolved. Monitor your credit report to verify the notation is removed if you used rehabilitation.

What Minnesota Borrowers Should Know in 2025

Minnesota has specific protections and resources worth knowing. The Minnesota Attorney General’s office actively monitors student loan servicer conduct and has challenged illegal collection practices. If you believe your servicer violated your rights during the default or collection process, you can file a complaint directly with that office.

Minnesota does not have a state income tax exemption specifically for loan forgiveness income in all circumstances – this matters if you’re pursuing forgiveness programs, because forgiven amounts may be treated as taxable income at the state level. As of 2025, borrowers should consult a tax or legal professional before finalizing any forgiveness strategy.

Borrowers in Minneapolis and surrounding Hennepin County communities including St. Paul, Bloomington, Plymouth, and Brooklyn Park often have access to nonprofit credit counseling and legal aid resources that can help assess options at no cost.

Required Documents Checklist Before You Call Your Servicer

- ☐ Your Federal Student Aid ID and login credentials

- ☐ Most recent loan statements from your servicer

- ☐ Proof of income (pay stubs, tax returns, or documentation of zero income)

- ☐ Employer contact information (in case of garnishment resolution)

- ☐ Documentation of any disability or financial hardship circumstances

- ☐ Copies of any collection notices received

Key Takeaways for Minnesota Borrowers in 2025

- Default triggers fast consequences – wage garnishment and tax seizure can begin without a court order

- Rehabilitation removes the default from your credit report – consolidation does not

- Income-driven repayment prevents re-default – enroll immediately after resolving default status

- Minnesota borrowers have AG complaint options – servicer misconduct can be challenged locally

- Getting legal guidance early saves money – collection fees can reach 16-25% of your balance if ignored

Frequently Asked Questions

How long does it take to get out of default on a federal loan?

Rehabilitation takes 9-10 months while consolidation can resolve default in 30-90 days. The timeline depends on which path you choose and how quickly your servicer processes the agreement. Starting the process immediately reduces how long collections can act against you.

Can my wages be garnished without a lawsuit?

Yes – federal loan servicers can garnish up to 15% of your disposable wages without filing a court case. This is called administrative wage garnishment and it’s unique to federal student loans. You do have the right to request a hearing before garnishment begins.

What happens to my tax refund if I’m in default?

The Treasury Offset Program can seize your entire federal tax refund to apply toward your defaulted balance. This happens automatically once your loan is referred for offset. Filing an injured spouse claim may protect a portion of the refund if you file jointly.

Does paying off a defaulted loan fix my credit?

Full repayment resolves default status but the history of late payments stays on your credit report for seven years. Rehabilitation is the only method that removes the default notation itself, which is why many borrowers choose it for long-term credit recovery.

Can I get into default again after rehabilitating my loans?

Yes, re-default is possible if you miss payments after rehabilitation or consolidation. Enrolling in an income-driven repayment plan with payments tied to your income significantly reduces this risk. Rehabilitation can only be used once in your lifetime.

Do I need an attorney to resolve loan default?

You don’t legally need an attorney to contact your servicer and enroll in a rehabilitation or consolidation program. But if you’re facing wage garnishment, a lawsuit from a private lender, or complex bankruptcy considerations, legal guidance from a firm like Hoverson Law Offices, P.A. in Minneapolis, MN can protect your rights and help you avoid costly mistakes.

Are private student loans handled the same as federal loans in default?

No – private lenders must sue you in court before garnishing wages, which gives you more time to respond. Federal loans allow administrative garnishment without a lawsuit. Private loan default options are more limited and vary by lender contract terms.

What This Means for You Right Now

Default feels like a dead end. It’s not. The system has built-in recovery paths, and people use them every day to stop garnishments, restore their credit eligibility, and get back to manageable payments.

The one thing that makes everything worse is waiting. Every month in default adds collection fees, extends credit damage, and reduces your options. Acting now – even just making one phone call to your servicer – starts the process.

If your situation involves wage garnishment already in progress, a lawsuit from a private lender, or questions about whether bankruptcy could discharge any portion of your debt, those are situations where having someone in your corner makes a real difference. Contact us today for straight answers about where you stand and what your next move should be. No jargon, no pressure – just a clear picture of your options.

For a complete overview of how we approach debt and financial legal matters, visit our services page.